The Value of Your Biggest Asset

Most assets that private business owners accumulate come from one source, their business. Owners can accumulate real property such as a primary home, a beach house or a ski house. They acquire furniture, cars, boats, or a jet ski. These assets are purchased either through salary or distributions earned from the business. The business is the source of revenue to fund all the expenses of the business owner.

The owners spend countless hours in their business. They plan, budget, forecast. They do all the necessary things to operate it efficiently and effectively. Time is spent on personal finances, planning for college and for retirement. Meetings are set up with the financial advisor, reviews assets and plans for the future. The house is appraised, the retirement plans counted, debt calculated, and net equity is arrived at. But, one thing is missing, the value of the biggest asset, the business. How can one plan for the future without knowing the value of the biggest asset? The business owner can ask themselves if any of these events will happen in the future.

- Retirement

- Sale of the business

- Passing it on to a key employee

- Passing it on to a child

- Death or disability

- Buyout of a shareholder

- Divorce

If the answer is yes, then a business valuation needs to be performed.

Some business owners feel the cost of a valuation is too expensive. Having a business valuation performed does not cost as much as one might think. For example, let’s say the cost of a valuation is $15,000. If the value of the business is $1,500,000, the cost of the valuation is only 1% of the total value. The chances any estimate of value is within $15,000 of the right value are slim. This means the best estimated guess needs to be within 1% of the right valuation. Costs are pennies on the dollar. I performed a business valuation for a business which had a value of $10 million dollars. Total fees were $25,000. That means the fee were .25% of the total value. Chances of using an incorrect valuation number (guess) for planning are high and risky.

Failure of not having a business valuation performed for your exit strategy can:

- Fail to provide for loved ones, by lack of adequate insurance.

- Cause scrutiny by the Internal Revenue Service, resulting in an audit.

- Under value the business during a sale.

- Over value gifts by not using discounts in the estate planning process.

- Result in expensive litigation with shareholders or shareholder’s heirs.

Appraisals of privately owned businesses are a complicated process. The purpose of the valuation, the valuation date, standard of value, the ownership interest, and numerous other factors all affect how a business is valued. To not have the valuation done by a professional or not done at all is irresponsible.

Every owner leaves their business. The question the owner needs to ask is; do you want to plan for the exit or do you want to roll the dice and gamble with the biggest asset in your portfolio?

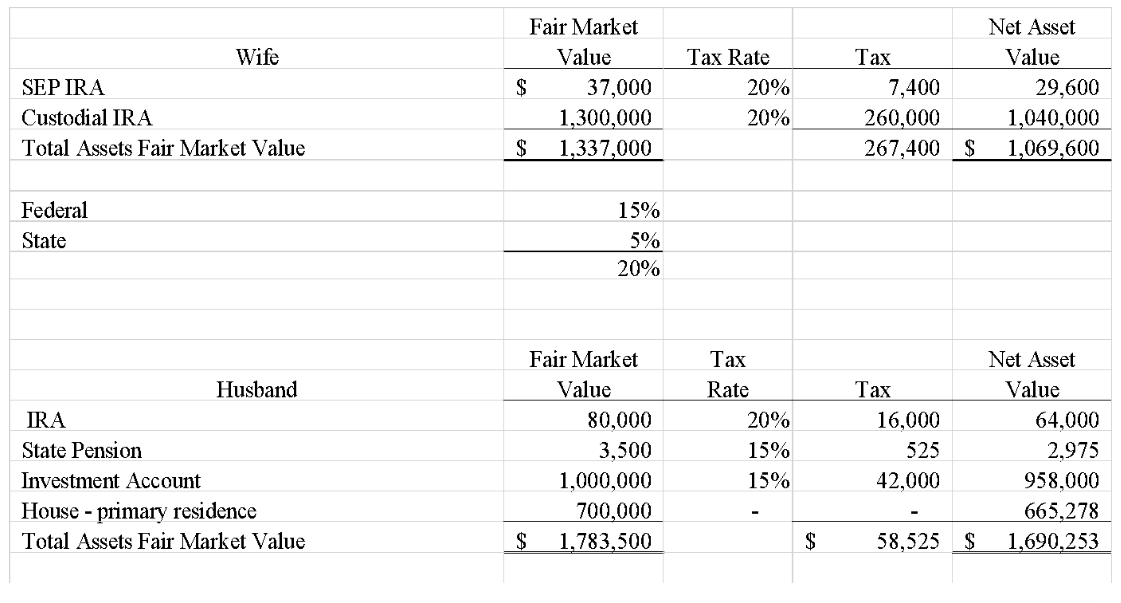

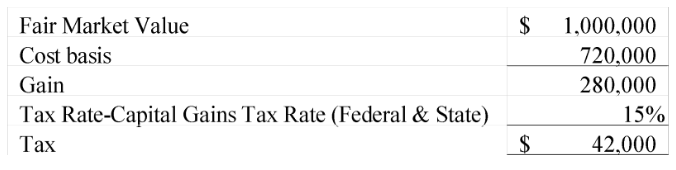

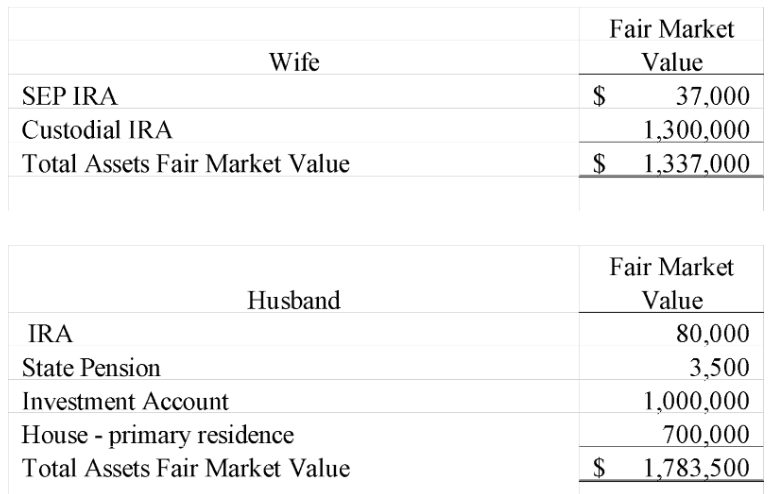

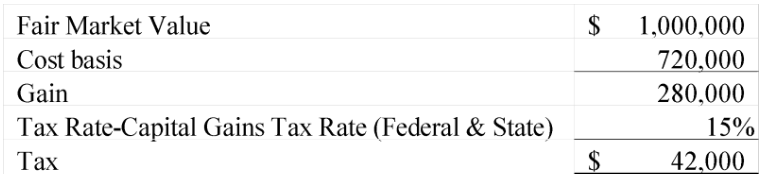

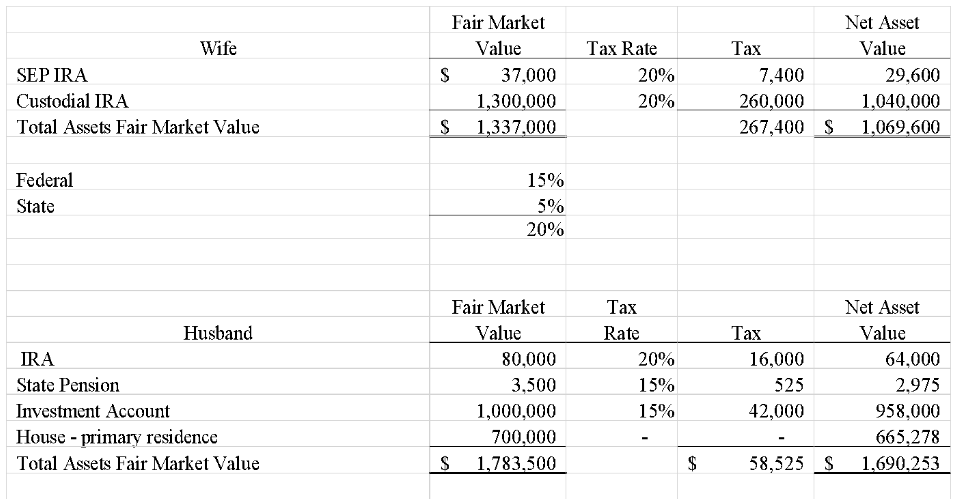

The divorce process can be stressful and emotional, particularly when dealing with financial decisions involving a family-owned business. A family business can either hold significant value as the largest family asset or simply function as a source of income, providing the owner with a job.

The divorce process can be stressful and emotional, particularly when dealing with financial decisions involving a family-owned business. A family business can either hold significant value as the largest family asset or simply function as a source of income, providing the owner with a job.