Divorce and Business

“Divorce can be one of the most stressful events in a person’s life next to the death of a loved one.” This is a pretty bold statement. I have also heard that a divorce is a business breakup. When one spouse owns or has an interest in a privately held business, the divorce process becomes even more complicated. Many issues arise that attorneys and divorce financial analysts need to be aware of.

VALUATION

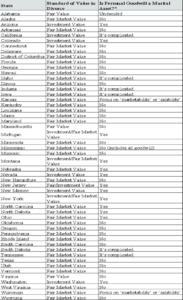

The first issue in a divorce when a business is involved is the value of the business. An interest in a privately owned business is a marital asset and subject to division. The way that business is valued is dependent on the state in which the divorce occurs. The method in which the business is valued is called the standard of value. For example, in Massachusetts the standard of value is case-by case-specific.1 For most valuations, Fair Value is the standard of value. Though there is no specific definition of Fair Value, it is Fair Market Value without discounts.

In Pennsylvania, Illinois, North Carolina and New Jersey, the standard of value is Fair Market Value. Fair Market Value is the amount at which the property would change hands between a willing buyer and willing seller when the former is not under any compulsion to buy. The latter is not under any compulsion to sell, with both parties having reasonable knowledge of relevant facts.

Some states are more complicated, like California, which defines the standard of value as value to the holder. The company may not have a market value for sale but the business’s value to the owner. For example, let’s have a sole proprietor who has net income on Schedule C – Profit or Loss From Business of $150,000. If the market salary for the industry for this owner is $100,000, they would have a $50,000 benefit for this business. A valuation analyst would then determine the value to the owner is the $50,000 worth, and that would be an asset divided in a divorce. However, some states have two standards of value. In New Jersey, the standard of value is Fair Value or Investment Value, and New York is Fair Market Value or Investment Value.

INVESTMENT VALUE INCOME

What a company reports on their financial statement or tax return for net income may not be the same as income used for income calculations for child support and alimony. These amounts need to be adjusted to account for discretionary expenses, generally accepted accounting principles and non-recurring income.

Expenses are challenging for “flow-through entities” such as S Corporations, Partnerships, Limited Liability Companies, and Limited Liability Partnerships. Some examples are:

- Discretionary expenses include owner’s compensation, rent paid to affiliates, auto expenses, charitable contributions, meals and entertainment, and country club dues. These items get added back to income based on their nature.

- Generally Accepted Accounting Principles (GAAP) – These adjustments could include converting the cash basis of accounting to the accrual basis of accounting, tax depreciation to GAAP depreciation, tax accruals, and other adjustments.

- Non-Recurring Items – These adjustments would include income and expenses that may have been only one-time occurrences, such as sales, legal expenses, bad debt write-offs, or forgiveness of loans such as Payroll Protection Program loans.

CONCLUSION

There are many issues involved when dealing with businesses than meets the eye. Attorneys and Divorce Financial Analysts need to use experts knowledgeable in these areas to ensure that the asset division and income calculations comply with the state-specific requirements and that proper accounting has been met.

1 Bernier vs. Bernier

*Source: BVResources.com as of April 2019.